Distributed consensus technology has a ton of interesting implications. It is fascinating how ecosystems and economies have evolved based on rules put in place by consensus algorithms, a reasonable system for storing history, and some shared belief of value.

The genius of open blockchains with a coin component is that different types of consensus function in unison to build trust without a central party.

I will be publishing a series of posts I am calling “stakeholders in consensus: how parties interact to create value in a blockchain ecosystem” to explore this concept. Stay tuned throughout the series to explore what it means for a blockchain to be decentralized, and who the players are that create value.

There are three categories of consensus that operate in parallel to make for a working open blockchain:

Components of each of these are largely interdependent and you can argue that different actors may participate in more than one of these. If any of these categories stop functioning as expected the others will also likely misbehave. We will explore some examples in a little bit.

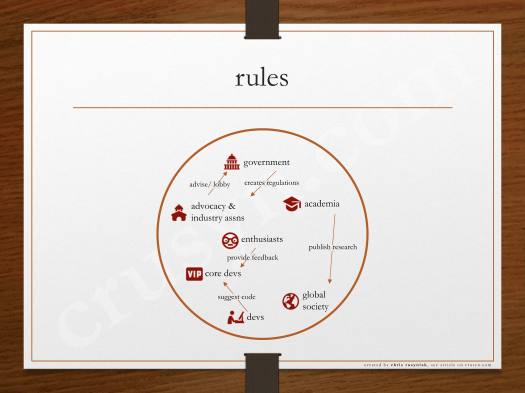

rules

Code is law! Well okay, that’s part of it. There are certain rules put in place by the system to make the system function. What immediately comes to mind are the rules for the actual consensus protocol. What makes a construct (transaction, state, execution, contract, or block) valid in such as system?

This can be extended to the greater universe in which a blockchain has to operate and this quickly becomes political. What rules are imposed on the ecosystem by governments? Who helps inform what the rules should be?

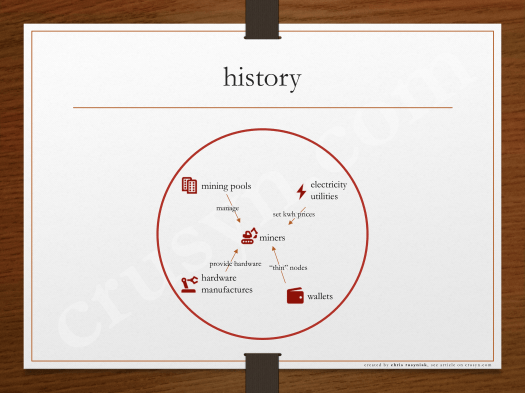

history

This is probably what most of us think of when we think of a blockchain, a long list of blocks that help us understand what happened in history. History (the blockchain, blocks, transactions, log entries) is important because it helps us understand who did what and how to arrive at the current state.

In the case of bitcoin and other utxo-based systems, it would be impossible to determine how much bitcoin a public key (address) controls without this transaction history. It would be impossible to detect malevolent behavior, such as double-spending, without this history.

What is interesting here is that history and the security of that history is impacted by network effects, internal economics, coin prices, and extrinsic factors like the price of electricity.

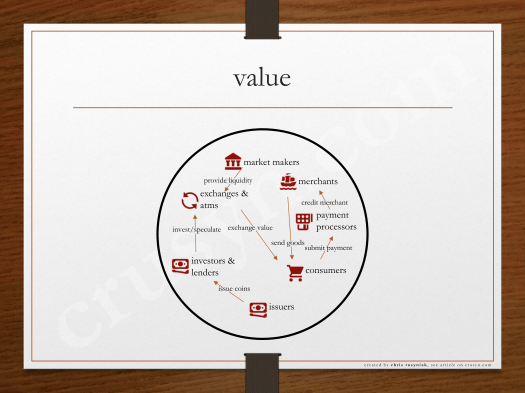

value

Lastly there must be consensus on value of the “coin” itself, or at least a relative range of values. This is again related to the rules since the economics are usually established there.

At the very simplest level the value of the coin is the value:

- at which one thinks someone will accept the coin in the future,

- the value of the use of a function of that coin to in the future,

- or the value of a stream of cashflows that that coin can produce for the holder.

We often get hung up on the specific value (i.e. price) versus another asset at a specific time and in a specific place. The value as described above may be different to different organizations or individuals. Furthermore, a coin having some value or range of values relative to another asset or service can be important, but is not critical.

If you have ever taken a Finance 101 class you know that value can be discounted to the present. We can use some discount rate based on the risk of whether or not you think you will actually realize that value and the amount of time before you realize it.

This form of consensus and the stakeholders involved should be very familiar to most, especially those with experience in capital markets. This is how paper and coin fiat money functions with “state” being the current holder of cash. We could talk for days about what gives fiat money value, and don’t fret, an article or two on that topic is forthcoming!

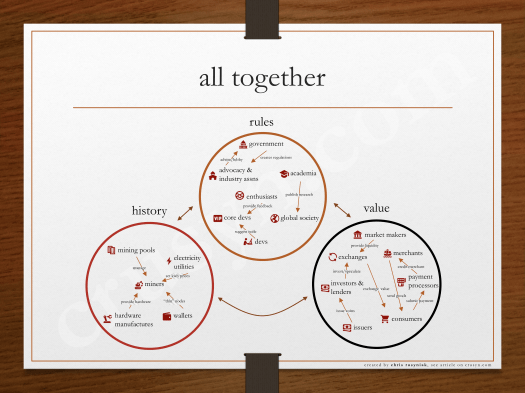

all together now

I’ll say it again: the genius of open blockchains with a coin component is that all three forms of consensus function in unison to build trust without a central party. The fact that parties are incentivized with a coin that will have value in the future to act fairly today is brilliant and underpins the whole system.

This is why many believe open blockchains built on open source will eventually overtake private systems as network effects and low friction make it more valuable and easier to transact in an open blockchain governed in a decentralized way forkable at any time. Contarily, a private system in the form of a database with a app (mediator, interface, API) layer on top or a private and/or permissioned blockchain is a closed system and doesn’t have the opportunity to evolve with its incentives in the same agile way.

Watch this space for future posts on details on the three forms of consensus, how they relate and interact, who the most powerful players are (hint.. the ideal is decentralization), blockchains as new public economies, as well as what defines a coin during and after a fork. The next article will be a deep dive on how rules evolve in distributed consensus.

attributions

I borrowed the original framework from the “Bitcoin and Cryptocurrency Technologies” Princeton course which is the best I have run into so far. Huge high-five to Arvind Narayanan, Joseph Bonneau, Edward Felten, Andrew Miller, and Steven Goldfederway for putting it together!

- arvind narayanan, et al: bitcoin and cryptocurrency technologies online course https://www.youtube.com/channel/UCNcSSleedtfyDuhBvOQzFzQ

Thank you to my partners Blake Johnson and Lane Rettig @ Crypto NYC as well as my brother David Rusyniak for providing feedback, content, graphics, and otherwise helping with this article series.

- blake johnson: thank you for your contributions and feedback

- lane rettig: thank you for your contributions and feedback

- david rusyniak: thank you for your graphic contributions and feedback

- crypto nyc: thank you for all your support!

http://www.cryptonyc.org

This article series was also inspired by debates and conversations had at BitDevs NYC. Thank you J and Max for putting that on!

- j and max: for inspiring sections of this series from their bitdevs nyc debates, socratic seminars, and conversations

https://www.meetup.com/BitDevsNYC/

- trace mayer: the seven network effects of bitcoin

https://www.weusecoins.com/the-seven-network-effects-of-bitcoin/

- icons8: icons in this document

https://icons8.com/